small")

Independent aftermarket shops across Canada each have their own customer base and approach to serving that market informed by the local demographics in terms of economics and busieness positioning.

And the experience of every ASP’s competitors is similar; from full car dealers to quick lubes — and even within the aftermarket among branded aftermarket shops displaying recognizable banners and those more clearly identified as independent, not overtly displaying any banner program identification, all have their own customer particulars to contend with.

Taken together though, all these thousands of annual service occasions do paint a picture of where Canadian car owners are bringing their vehicles and how much they’re spending.

In the Annual Aftermarket Intelligence Report produced by Jobber Nation and Indie Garage, we presented what we believe to be the most comprehensive Canadian research on this aspect of auto repair customer behaviour.

(For more market share data by key service categories and more, check out the full Aftermarket Intelligence Issue HERE)

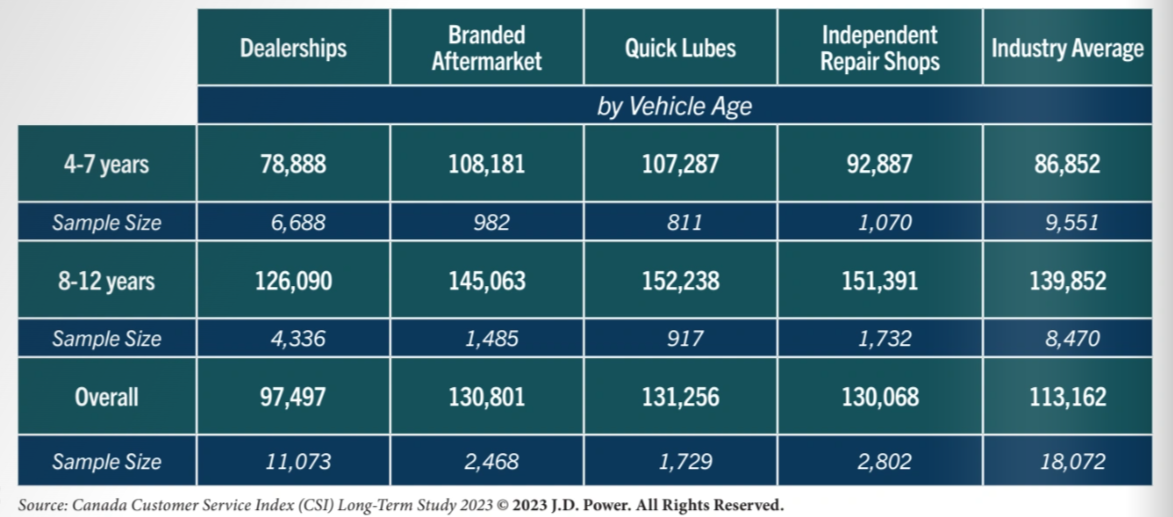

Average Kilometer Reading

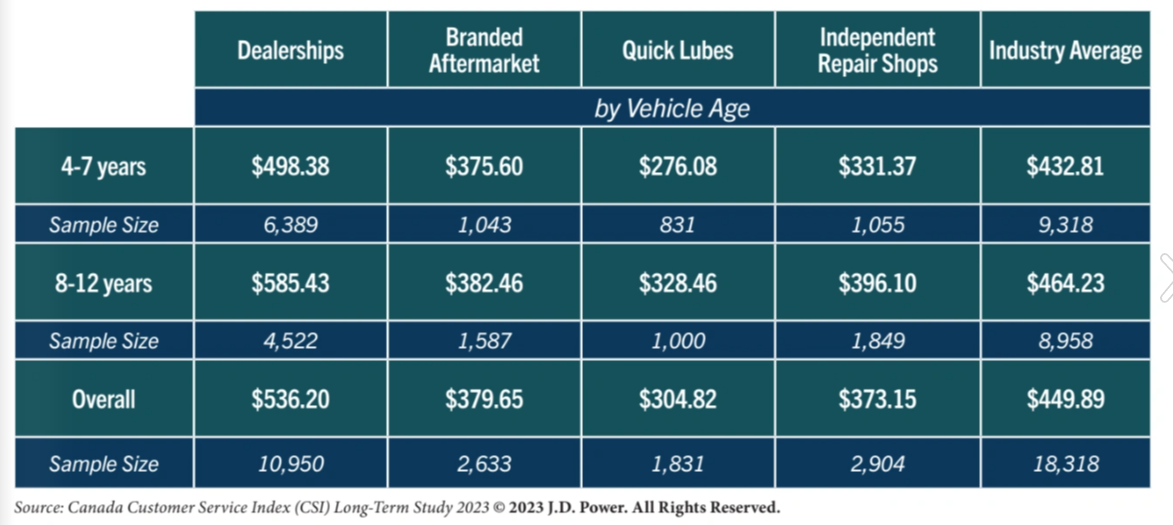

Average Bill by Vehicle Age

TREND TO WATCH: OVERALL SERVICE MARKET RETURNS TO “NORMAL”

The overriding trend over the past year for the automotive service sector in Canada as a whole is what can best be described as a pullback to more normal total dollars.

While during the depths of the pandemic there were erratic shifts and changes in both activity and where that service activity took place—independent automotive service providers did particularly well as competing car dealer fixed-ops struggled relatively more with restrictions and capacity constraints—with a high-water mark of more than $10 billion CAD in service business.

In 2023, that total volume dropped down to approximately $9.1 billion CAD, which is more in keeping with pre-pandemic activity estimates.

Despite this “normalcy” however, this is still activity executed against headwinds of both inflationary pressures and demands on consumers, and continuing—if moderating—supply chain challenges.

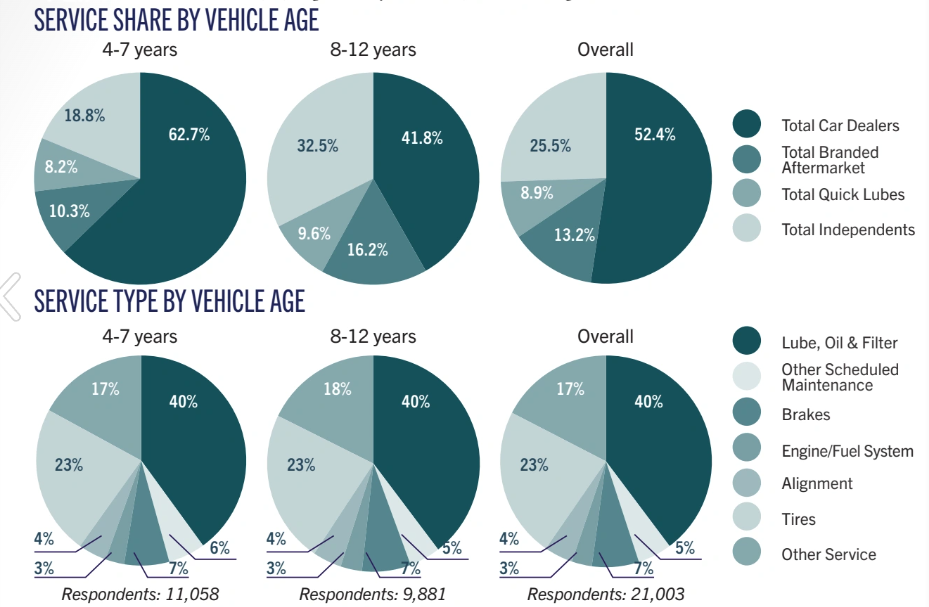

Within the numbers provided by JD Power through the Customer Long Term Service Index tracking vehicles 4 to 12 years old, the Independents continued to have the majority of service occasions, while having slightly below half of the service dollars.

Additional research data indicates strong miles driven continuing, inflation moderating, and ongoing improvements in supply chain performance that together indicate opportunities for improving performance ahead.

Check out the rest of the Aftermarket Intelligence Issue digiial edition

0 Comments